The scandal at the Vatican bank

On June 28 this year, Italian police arrested a silver-haired priest, Monsignor Nunzio Scarano, in Rome. The cleric, nicknamed Monsignor Cinquecento after the €500 bills he habitually carried around with him, was charged with fraud and corruption, together with a former secret service agent and a financial broker. All three were suspected of attempting to smuggle €20m by private plane across the border from Switzerland. Prosecutors alleged that the priest, a former banker, was using the Institute for Religious Works – the formal name for the Vatican’s bank – to move money for businessmen based in the Naples region, widely regarded in Italy as a haven of organised crime. Worse still, Scarano (who, together with the other men, has denied any wrongdoing) had until only a month earlier been head of the accounting department at the Administration of the Patrimony of the Apostolic See, the treasury of the Vatican. The arrest, and the headlines that screamed across the Italian press, was the latest shock for the Holy See.

How God’s bank ended up as a financial penitent this year is a bracing chapter in the history of financial reforms that have swelled up in the aftermath of the 2008 credit crisis. Untouchable havens such as Switzerland and Liechtenstein were forced to open their chocolate-box palaces to the probes of international regulators. This year the power of the popes was challenged. The FT interviewed two dozen bankers, lawyers, regulators and Catholic insiders over 11 months to understand how the murky operations of a bank with €5bn in assets, and which says its aim is to serve the global mission of the Catholic Church, had unnerved bankers, regulators and governments across Europe and the US. The reforms now under way at the Vatican have come about in part because of the pressure brought to bear by banks such as Deutsche Bank, JPMorgan and UniCredit, all of which found themselves in the sights of regulators because of their business relationships with the Holy See.

Several financial professionals talked in detail to the FT about their dealings with Vatican staff and provided documents about the bank’s structure. None wanted to speak on the record, citing sensitivities in both their banking and religious worlds. All told the FT that they were speaking out in order to help the bank keep to its programme of reform. Senior executives from some correspondent banks had been questioned by regulators over the past two years and several had the same refrain about their dealings with the Vatican bank: it operated unlike any other bank they had encountered. Some who spoke to the FT reinforced what later emerged from reports by European officials on the bank’s workings. There were surprisingly few checks and balances on cash flow – and far less documentation than expected.

Several financial professionals talked in detail to the FT about their dealings with Vatican staff and provided documents about the bank’s structure. None wanted to speak on the record, citing sensitivities in both their banking and religious worlds. All told the FT that they were speaking out in order to help the bank keep to its programme of reform. Senior executives from some correspondent banks had been questioned by regulators over the past two years and several had the same refrain about their dealings with the Vatican bank: it operated unlike any other bank they had encountered. Some who spoke to the FT reinforced what later emerged from reports by European officials on the bank’s workings. There were surprisingly few checks and balances on cash flow – and far less documentation than expected.

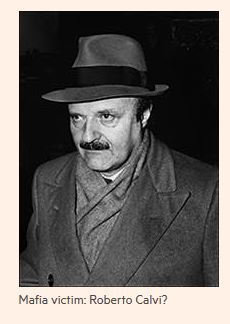

The most infamous publicity surrounded revelations about the Vatican bank’s dealings with Milan’s Banco Ambrosiano, one of the most high-profile bank collapses in Italy’s history. The Vatican bank was Banco Ambrosiano’s main shareholder. After its demise in 1982, Banco Ambrosiano’s chairman, Roberto Calvi, was found hanged under London’s Blackfriars Bridge. Prosecutors in Rome concluded that he was killed by the Sicilian Mafia but no one has ever been convicted of his murder. In recent years, the bank has again featured in media reports for its funding of religious and humanitarian activities across the world. Former and current Vatican officials have confirmed to the FT that the bank has been used to channel cash, often secretly or with limited information given to correspondent banks, to vulnerable Christian groups in Cuba and Egypt. But Vatican insiders, bankers and prosecutors admit that a system aimed at quickly getting money to difficult places has also potentially been open to abuse by tax cheats and by organised crime.

The most infamous publicity surrounded revelations about the Vatican bank’s dealings with Milan’s Banco Ambrosiano, one of the most high-profile bank collapses in Italy’s history. The Vatican bank was Banco Ambrosiano’s main shareholder. After its demise in 1982, Banco Ambrosiano’s chairman, Roberto Calvi, was found hanged under London’s Blackfriars Bridge. Prosecutors in Rome concluded that he was killed by the Sicilian Mafia but no one has ever been convicted of his murder. In recent years, the bank has again featured in media reports for its funding of religious and humanitarian activities across the world. Former and current Vatican officials have confirmed to the FT that the bank has been used to channel cash, often secretly or with limited information given to correspondent banks, to vulnerable Christian groups in Cuba and Egypt. But Vatican insiders, bankers and prosecutors admit that a system aimed at quickly getting money to difficult places has also potentially been open to abuse by tax cheats and by organised crime.

A routine Bank of Italy anti money-laundering investigation at the branch had stumbled upon inconsistencies in its dealings with the Vatican bank, and it referred the issue to Rome prosecutors. According to a source familiar with the matter, payment slips from unnamed holders of Vatican bank accounts were found in the branch, ringing alarm bells for anti-money laundering investigators. The investigation was shelved later that year but not without consequences for the Vatican. UniCredit says it cut off all contact with the Holy See. It would not be the last bank to do so. Forcing change was a challenge. Part of the problem was that the European Union had no regulatory power over the Vatican’s bank. So it was decided that the Bank of Italy, at the time headed by Draghi, would put pressure on the banks that did business with the Vatican. A former Italian minister with direct knowledge says: “That is the way you do it in these situations, when you have a state that you do not have regulatory powers over but you want to enforce changes.

A routine Bank of Italy anti money-laundering investigation at the branch had stumbled upon inconsistencies in its dealings with the Vatican bank, and it referred the issue to Rome prosecutors. According to a source familiar with the matter, payment slips from unnamed holders of Vatican bank accounts were found in the branch, ringing alarm bells for anti-money laundering investigators. The investigation was shelved later that year but not without consequences for the Vatican. UniCredit says it cut off all contact with the Holy See. It would not be the last bank to do so. Forcing change was a challenge. Part of the problem was that the European Union had no regulatory power over the Vatican’s bank. So it was decided that the Bank of Italy, at the time headed by Draghi, would put pressure on the banks that did business with the Vatican. A former Italian minister with direct knowledge says: “That is the way you do it in these situations, when you have a state that you do not have regulatory powers over but you want to enforce changes.

Bruelhart worked swiftly to restore ATM services in Vatican City. By February 12, he had engaged Aduno Group, a Swiss company, to take over operation of the cash machines, neatly circumventing Italian and EU regulatory pressures. In March 2013, there was a new pope – a Jesuit evoking the poverty and humility of St Francis of Assisi – and he quickly set a tone on financial correctness. Pope Francis spoke out against the “idolatry of money”, “all-encompassing corruption” and “tax evasion that had reached global dimensions”. Behind the scenes, he sent out another sign: Pope Francis moved his personal residence away from the Apostolic Palace and the Vatican bank. Francis also began issuing papal decrees that helped speed inspections and made changes within the upper ranks of the cardinals. According to Bank of Italy sources, the new pope “marked important steps toward real reform of the legal and institutional framework”. Backed by Francis, the Financial Information Authority was strengthened with broader powers of supervision.

By this summer, von Freyberg had sought out Promontory Financial, a global risk-control group that specialises in regulatory and compliance issues. Promontory’s contract, according to von Freyberg, costs “well above seven digits”. On a bright morning in late October, nine Promontory Financial employees sat in an office beneath a painting of the crucifixion of Christ, sorting through computer scans of account holders’ passports. They were manually and methodically cross-checking the names and faces with newly filled-in bank forms. Promontory employees now comprise 25 per cent of the staff of the Vatican bank, according to the Vatican. Next door sat Rolando Marranci, a former chief financial officer for BNP Paribas’s Italian subsidiary and now the Vatican bank’s new director-general. He was hired in the wake of the arrest of Scarano, the Vatican accountant.

By this summer, von Freyberg had sought out Promontory Financial, a global risk-control group that specialises in regulatory and compliance issues. Promontory’s contract, according to von Freyberg, costs “well above seven digits”. On a bright morning in late October, nine Promontory Financial employees sat in an office beneath a painting of the crucifixion of Christ, sorting through computer scans of account holders’ passports. They were manually and methodically cross-checking the names and faces with newly filled-in bank forms. Promontory employees now comprise 25 per cent of the staff of the Vatican bank, according to the Vatican. Next door sat Rolando Marranci, a former chief financial officer for BNP Paribas’s Italian subsidiary and now the Vatican bank’s new director-general. He was hired in the wake of the arrest of Scarano, the Vatican accountant.